Do you have payments in your veins?

Big week for challenger banks with updates from Monzo, Starling, Current and news from Google getting involved. Earnings from Square, vein-mapping payments FinGo gets a green light in Manchester (UK) and a scaling back of Uber’s financial service ambitions. And Pulse, startup of the week!

If you enjoy reading this, please subscribe and share with your family, friends and other fintech enthusiasts!

Recent News 📰

CNBC reports that Goldman Sachs has made Mathew McDermott, MD in the internal funding operations, its new global head of digital assets. This signals the intent of GS in the digital asset space as he has strong views on moving financial assets to electronic ledgers powered by blockchain.

FedNow is still on track for 2023/2024 according to Lael Brainard. The real-time payment and settlement system will also include fraud and liquidity tools. Covid has highlighted the need for such systems and there are 100 people currently working on it. I wonder would a startup be able to deliver something quicker?

Capital One is paying an $80m fine for a 2019 hacking incident that caused the personal data of 100m Americans and 6m Canadians to be compromised. A pitiful $0.75 slap on the wrist per impacted customer. Not that they get to see any of the money. Small fines like this really don’t do anything to encourage banks to take data security seriously, especially with the bank not admitting or denying the allegations. It would be great to see a stronger response from regulators and possibly a flat $10 fine per impacted user.

ComplyAdvantage has announced a $50m Series C round for expansion, led by Ontario Teachers and previous backers Balderton and Index. With more and more financial services shifting to digital, there will be a consumate increase in financial crime and ComplyAdvantage has developed an AI platform and databases of 10m entities to help identify and track financial crime. Also another example of funding from a non-traditional source (i.e. Ontario Teachers)

DOJ is investigating Intuit’s acquisition of Credit Karma, potentially signalling a rough ride for approval of the $7bn transaction on anti-trust grounds. Credit Karma currently has a free tax filing product which competes with Intuit’s product which costs between $60 and $100 and has 67% market share. Intuit could easily wipe out a free alternative leaving customers in a worse position so hopefully there is some remedy here.

The Transferwise mafia is growing, with former Transferwise employee Mart Abramov and MarketInvoice alumni launching a self-assessment tax tool, TaxScouts, for the UK and Spain markets. The company has just raised £5m for a Series A led by Octopus Ventures.

Banks across the globe are struggling to combat financial crime, with anti-money laundering fines in 2020 already surpassing those of 2019 according to Duff & Phelps. 2019’s total of $444m has easily been beaten by $706m so far this year.

Challenger Banking 🚀

Google announced more details of its upcoming digital banking service, with new co-branding partners to include Bank Mobile, BBVA, BMO Harris, Coastal Community Bank, First Independence Bank and SEFCU, joining already announced Citi and SFCU. Google has targeted a range of banks to increase penetration with customers. Google is reported to be providing the consumer front end and the banks do the back end lifting. Google is offering banks a co-branding experience which will help allay their fears of being relegated to a behind the scenes function. This is a different approach than what Apple seems to be pursuing. Apple will try and own the mobile payments space, hence its recent acquisition of Mobeewave, whereas Google is looking to get deeper into financial services. Both are huge data plays as you would expect.

After PayPals earnings last week, Square reported earnings last week which exceeded expectations and sent shares up 9% after hours. Square had $1.92bn in Q2 revenues (+64% yoy). Cash App gross profit +167% yoy to $281m and stored funds +86% qoq with 30m users. However it wasn’t all smiles as its core seller business profits -9% yoy and GPV -15% yoy.

Monzo reported last week and it was Starling’s turn this week. ARR increase +370%, to £80m and set to be profitable this year. Starling has 1.5m accounts in total, with business accounts doubling to 200,000+. Starling managed to increase customer deposits and lending from £1bn and £54.2m in November 2019 to £3bn and £1bn by July 2020. (Side note; spending per customer has bounced from £330 to £264 but back up to £350 through the covid period.)

The BoE asked Monzo to increase their regulatory capital to 13.6% of RWA, up from 9% previously as the central bank looks to be getting tougher with fast-growing fintechs. It remains to be seen as to what increase the BoE have asked of Starling, if any.

US challenger bank Current has jumped on the bandwagon of providing rewards for using your checking account/debit card. They are launching a points program, rewarding members with 15x points on debit purchases at 14,000 merchants including Subway, Rite Aid and True Value. Points will be redeemed for cash at 100 points per $1.

Spain’s challenger bank Bnext increased its €22m Series A by a further €11m. The company has attracted 300,000 active users and uses an E-money license.

Sync, a PFM and bank aggregation service started by a former Revolut employee has announced a £5.5m seed round. Sync adds its name to a long list of PFM apps offering similar functionality, most of which have struggled to monetise. Differentiating features for sync seem to be to be the ability to exchange currencies between accounts, unsure how useful that is, and to generate a unique CVC number via the app. Investors include Alibabam Jumpstarter HK, Wayra UK and T12M.

In a surprising move the UK Competition and Markets Authority blocked FNZ’s takeover of rival GBST, saying that it could lead to worse outcomes for British investment customers.

Fintech Infrastructure

Back in June, the UK Government picked TrueLayer to supply its payment initiation service (PIS) to public sector organisations. This is a huge win for the company and potentially the tax payer due to the savings on transaction fees.

The US and UK are not the only places developing payments infrastructure for incumbent players, Brazil based Swap has raised a $3.3m seed round to improve technology innovation at financial institutions. The round was led by ONEVC and included names such as Flourish Ventures, Hustle Fund and GFC.

Payments 💰

UK based FinGo has announced its vein-mapping identity and payments technology is to be used in a bar and restaurant in Manchester. A user creates an account with FinGo which verifies their age and identity and adds a payment card to their profile. Establishments get a FinGo reader which can be used to check ages, contact customers as part of track and trace Covid program and to settlement the bill. The establishments don’t get customers data providing another level of security for customers rather than handing over your driving license for identification which is increasily being scanned into a database.

Germany banking giant Commerzbank has had to write off €175m in loans to Wirecard with the total impact on all its lenders up to €1.8bn.

A further developments in the Wirecard scandal shows that they were fined heavily by Visa and Mastercard for miscoding gambling transactions, high levels of stolen card purchases and chargebacks. The scandal appears like an onion with many layers going very deep. I am sure this story will continue to unravel for months to come.

Curve plans to launch a rival to Klarna this year, named Curve Credit and is targetting 300,000 customers within three years.

Also in the installment/BNPL space was Splitit raising $71.5m. Splitit enables shoppers to pay in instalments using their credit card, a potentially easier concept for shoppers to grasp rather than getting loans at checkout.

Strong Customer Authentication (SCA) has led to higher cart abandonment according to Microsoft. SCA demands 2-step verification for purchases in Europe greater than €30. Concerns about this and impacts of Covid have led UK to delay imp-lementation but the EU is pressing ahead with merchants set to lose out even more.

Embedded Finance

Uber is reportedby scaling back its financial services efforts, according to Ron Shevlin at Forbes. CEO Dara Khosrowshahi is stopping credit card, digital wallet and instant payment projects to refocus on its core business. Uber had the potential to play a large role in embedded finance and to capitalise on its close relationship with drivers and the data it has on their earnings. A future where a driver could be paid in real time and borrow money from Uber who assesses them based on their work history, looks to be a lost cause now.

Grab, the South East Asian super app has launched more financial services, further embedding itself into users lives. The new offerings include a micro-investing platform, consumer loans and buy now pay later checkout options with certain merchants.

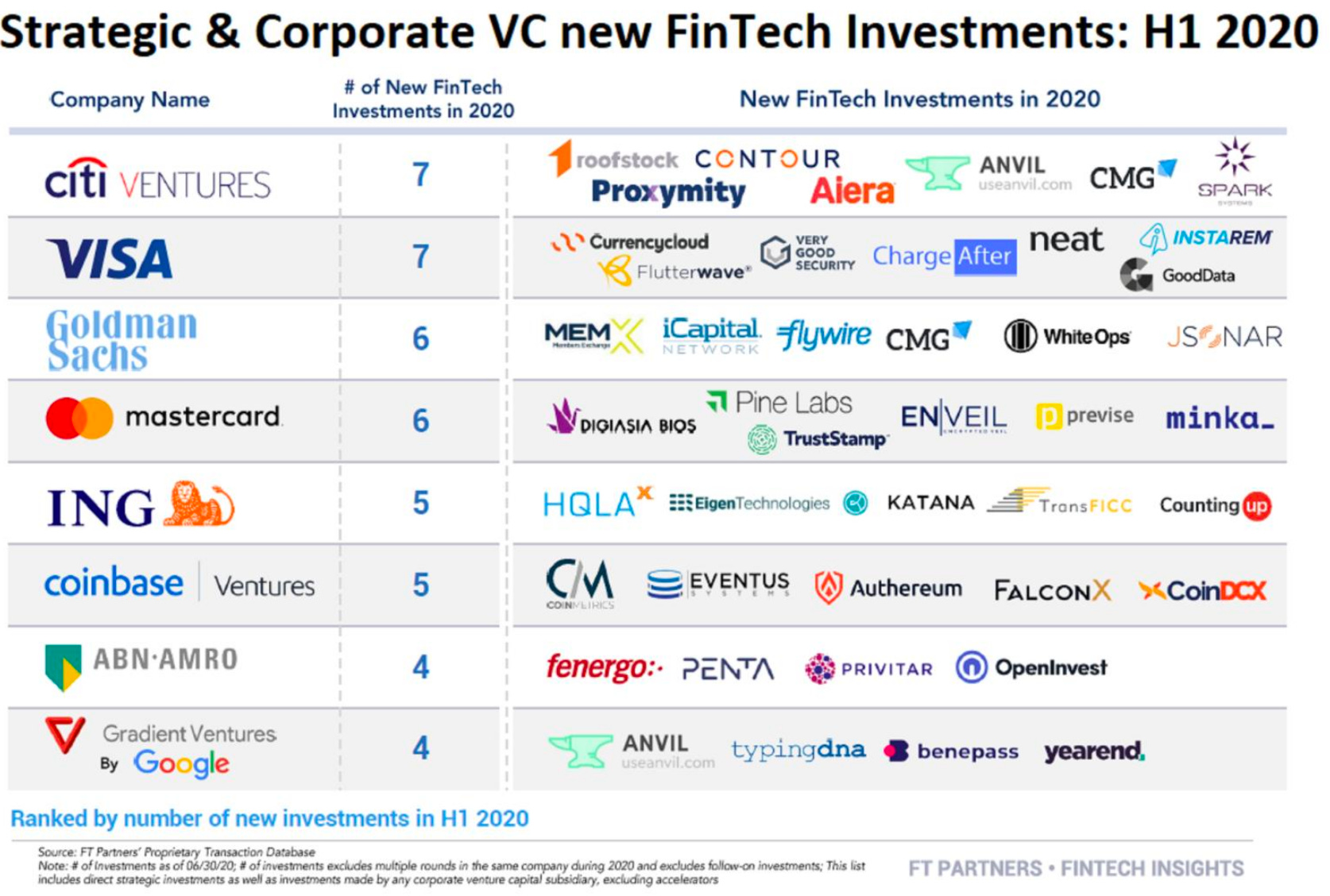

Strategic and corporate VC investments for H1 2020 from FT Partners

Longer reads 📜

With consumers under increasing financial pressure due to the pandemic, debt collection is having its time in the sun with new technologies being developed to make collection more efficient, conversational and humane. American Banker reports on some interesting developments and features startup TrueAccord.

Analysis of Apple’s acquisition of Mobeewave here, here and here.

Is a sixty year old programming language best to run most financial services? Chris Skinner’s take.

a16z on Fintech and vertical SaaS

Startup of the Week ⭐

Pulse is a UK based fintech startup that allows companies to get access to their annual SaaS revenue quickly to provide much needed capital to grow. A form of revenue based financing that is becoming more popular for SaaS style businesses which reduces the need for traditional VC financing and the subsequent dilution and loss of control.

Co-founder Nathan Pamart is formerly of Bain Capital, BCG and Energy UK. The company has yet to announce any funding.

Please get in touch to share your thoughts and comments!

Follow me on LinkedIn and Twitter.

Michael