FATP Special - 99 problems and my employee’s finances are one.

Employers should care about their employees wellbeing, if not out of compassion for others, then for the impact it has on their business. Employee stress is proven to lower productivity and decrease employee retention causing businesses a significant cost, estimated at $500bn in the US alone. An increasing driver of this stress is employee’s financial wellbeing but this is a burgeoning area that fintechs are tackling, so there is hope.

1. The scale of the problem

The core mission of the Consumer Financial Protection Bureau (CFPB) is to empower consumers to take control over their financial lives. It defines financial wellbeing as;

“a state of being wherein a person can fully meet current and ongoing financial obligations, can feel secure in their financial future and is able to make choices that allow them to enjoy life”

In order to empower, in late 2016 they commissioned a nationwide survey of US adults and measured financial wellbeing on a range of different metrics and some of the findings are below;

The median financial wellbeing score for US adults was 54 on a scale from 0 to 100

A third of adults have a score less than 50, which is associated with a high probability of failing to make ends meet.

Scores were aligned with the amount of liquid savings and point to the importance of savings in feeling financially secure.

Unsurprisingly, high levels of financial literacy have strong positive relationships with financial wellbeing.

No difference in wellbeing based on region or gender and differences due to race or ethnic groups is small.

Adults who had experienced negative financial incidents e.g. rejected for credit, contacted by debt collectors, have lower wellbeing scores.

2. No financial safety net

The survey pointed to the existence of a financial safety net as being the core driver of improving financial wellbeing, which predominantly includes savings and retirement income. It clearly demonstrated that wellbeing was more related to having such a safety net rather than being an income specific phenomenon.

When combined with the FDIC Survey of US Family Finances which found that in 2019 only 59% of families saved, it demonstrates how significant the problem is. A 2019 survey from GOBankingRates found 45% of respondents had $0 savings and 24% had less than $1,000. The number of respondents that had less than $1,000 in savings has shot up compared to 2017 when it was 57%.

There is a similar situation across the pond according to the Financial Lives Survey from the Financial Conduct Authority (FCA). The survey from 2017 found;

57% of UK adults had no savings or less than £5,000 saved

71% had no investments

31% had no private pension

26% had no savings or investment product.

The findings illustrate that over 50% of the UK adult population show characteristics of financial vulnerability, which include low financial resilience and over-indebted. 42% of UK adults are dissatisfied with their financial circumstances and only 21% are highly satisfied. Only 37% are confident in managing their money with 16% saying they feel highly knowledgeable.

Not only is it a problem that consumers in the UK and US both have little in terms of a financial safety net but it can also cause a death spiral.

Source: Salary Finance

Salary Finance found that 32% of people regularly run out of money between paychecks regardless of their level of financial stress but increases to 56% if they are financially stressed. This can turn into a financial death spiral as to make ends meet, consumers take out expensive unsecured credit to bridge the gap, whether that is credit cards with 20% interest or worse still, payday loans with 400% average interest rates.

Interestingly, there is a gender disparity in worrying about finances, although no difference in actual wellbeing as found in the CFPB survey. 41% of men according to Salary Finance worry about their finances but 51% of women do. For the other worries mentioned, health, relationships and career, there was a less of a gender gap.

3. Psychological Impact

This sad state of personal finances has big consequences for consumers.

In both the US and the UK, consumers are worried about their financial situations. Money was the biggest stress cause in the UK according to Perkbox and the APA found 72% of Amerians are stressed about money. This data is backed up by PWCs annual Employee Financial Wellness Survey 2020, which found 48% are distracted by money worries at work and 38% can’t sleep at night due to financial concerns. The knock on impacts of financial stress are profound, with those people 6x more likely to suffer from anxiety and 7x more likely to suffer from depression.

This stress has a very real impact on the workplace. Stressed workers are preoccupied with their problems and have lower productivity and also increased absenteeism. This comes from lack of sleep, excessive consumption of drugs and alcohol as well as physical health implications from stress such as high blood pressure, heart problems, weight issues, sleep disorders and memory loss.

4. Employers take note

The psychological impacts of financial stress manifests itself in employees productivity and retention which are two costly issues for employers.

According to PWC, financial stressed employees are 5x more likely to take time off to deal with personal issues and Salary Finance found they are 2.2x more likely to leave, almost 6x more likely to not finish daily tasks and 4.3x more likely to have bad relationships with colleagues. The estimated lost productivity days are 29–39 per year.

Research from AXA, the insurance company, found 5% of individuals admit to having taken time off work as a result of money worries and 35% believe they are not performing at their best because of financial concerns. An Aon survey found 70% would like more support from their employer when it comes to their financial situation.

The financial cost to employers in the US of this loss in productivity and employee turnover account for 11%-14% of payroll expense, which is $500bn in the US annually. To put that amount into context, it’s equivalent to almost 7% of government spending and 2.3% of GDP. The Centre for Mental Health found that the overall cost to British employers of stress, anxiety and depression was £1,035. Absenteeism was 32% of the cost, presenteeism was 58% and 9% was due to churn. They put the total cost to UK businesses at nearly £35bn

5. What do solutions look like?

Financial wellness programs have been shown to partially address employee retention and productivity.

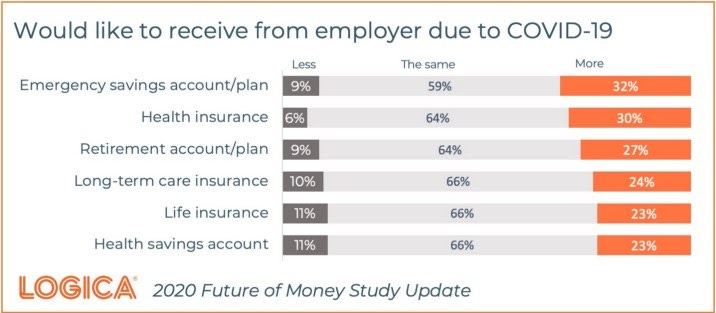

Since COVID struck, employees have come to expect more from the employers as well. The 2020 Future of Money study from Logica found emergency savings as the service employees would like more of from their employers.

The first part of the solution is to properly diagnose the problem. According to research, around 53% of companies surveyed employees in the past year and 45% have done annual surveys for the past three years however they don’t always focus on financial wellbeing. It is critical to spend the time to properly understand where your employees are at, what they are struggling with and what they need help with.

Given the survey outcomes, it is clear that building up a financial savings safety net is one area that solutions should focus on as well as helping plan for retirement and reducing the reliance on expensive short term credit.

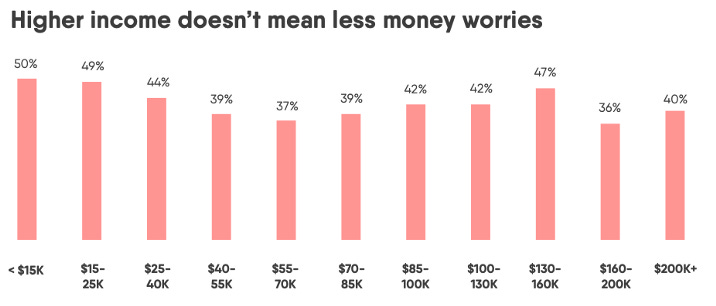

For the purposes of this analysis, increasing pay is out of scope. This is due partly to the complex nature of the issue and the associated political perspectives, but also because most research indicates there isn’t a great decrease in financial stress with higher incomes. The data from Salary Finance on this is below.

Financial safety net

Having liquid savings, as described earlier, can lead to employees feeling more financially secure. Whilst the level of savings will be subjective based on the unique circumstances of each individual, the research indicated that consistently saving can help to reduce stress.

One way of increasing the level of liquid savings for employees is to provide access to a financial advisor. Salary Finance found that this was consistently one of the top three desired benefits for respondents across the spectrum of financial wellbeing. With most people asking family and friends for financial advice and recommendations, combined with online research, there is a lack of confidence still. Finances are still seen as a scary topic and although people rely on friends and family, there is a lack of trust and confidence in their recommendations and a perception that they do not have enough to invest. However over the past, access to investments has greatly been democratised.

Part of being able to save more is budgeting. Salary Finance survey found that employees have a core knowledge about good financial habits and know how to budget but the problem is sticking to them. Only 55% of those with low financial wellbeing understand the concept of financial goals.

In order to build a safety net, employers need to encourage employees to save. One way to do this is to auto-enroll employees in a savings plan and get them to save a set proportion of their salary each month into an existing or provided savings account. This taps into the concept of Save More tomorrow developed by Nobel Prize winner Richard Thaler and Shlomo Benartzi. In their paper “Save More Tomorrow™: Using Behavioral Economics to Increase Employee Saving” Thaler and Benartzi demonstrate that 78% of those offered a plan to commit in advance a portion of their future salary increases towards retirement savings actually enrolled in the plan and 80% remained through the fourth pay rise. Auto-enrollment would go some way to combating the almost half of Americans who are not ready for retirement according to Economic Policy Research.

This is backed up by survey data as well from Salary Finance.

Short term credit

Given that almost a third of employees run out of money between paychecks and they are increasingly turning to expensive forms of short term credit, providing them an alternative is another way to improve their financial wellbeing.

Two options here are salary linked loans and access to earned income. Many startups such as Wagestream, PayActiv, Earnin etc have popped up in this space and allow workers access to their salaries earlier than payday and sometimes as they are earnt, which removes the need to borrow at expensive rates. Salary Finance provides loans to employees that are linked to their paycheck and can be a cheaper source of credit because they come out of the paycheck directly. They found that its loan benefits have increased retention by 28% and employees have saved two thirds in interest payments.The benefit of salary linked loans was confirmed by Harvard professors Todd Baker and Snigdha Kumar in their 2018 paper.

6. Startups working in this space.

There are many startups increasingly working in this space but often on one solution in isolation. There are many startups providing earned income access (EIA), many providing education and many providing advice. There are not many providing a holistic and personalised approach to the problem. Northstar, Origin and Brightside are platforms that take this comprehensive approach.

Northstar

Northstar was founded in 2016 by engineer Matt Matteson and product/venture capitalist William Peng. It provides personal financial management features such as account aggregation with 1:1 advice from experts to make the insights that are recommended actionable. This aggregation of accounts is unique to other companies in the employee financial wellness space which I like and provides more data and insights relevant to holistic financial advice. They have also developed an automated system for moving money based on goals and use concepts developed by Nobel Prize winner Richard Thaler to encourage responsible behaviour.

Membership can be provided through an employer or costs $25 per month directly. Northstar definitely takes a more consumer approach than the other platforms and looks more like a personal financial management app and sells via B2B channels as well. Would love to see salary linked financial services offered as well that have been mentioned earlier.

Origin

Origin is a financial wellbeing platform that helps companies relieve employee financial stress. Origin provides personalised financial plans and partners with top financial service providers who can put plans into action. The key to its offering is that the advice it gives is not generic like employees can find on the internet. It is specifically tailored to each employee’s financial situation and goals.

The company was founded in 2018 by Matt Watson and Joao de Paula. Matt has a background in finance and is a former co-founder. After his move from Citibank in New York to San Francisco to start his first company, he encountered the financial stress associated with early stage startups and the problem stuck. Joao is the CTO and was the first brazillian to be accepted into YC in 2013. He co-founded his own startup prior to Origin and built that out over seven years.

In June Origin raised $12m from VCs and reported it had 15 customers with between 250 and 5,000 employees. Companies pay $6 per employee per month. This would put ARR in the $270k — $5.4m range. It recently released Origin 2.0 in August which provides unlimited planning with a Certified Financial Planner.

Brightside

Brightside is another similar platform providing a personalised network of financial solutions for employees. Brightside also offers access to financial assistants to help. Brightside doesn’t make money from consumers, any referral fee it gets is passed back to consumers. The company was founded by Shawn Leavitt, an innovator in employer benefits, in 2017 and has raised $41m to date. Its latest Series A round was completed in June 2020 at a valuation of $120m. Investors in the company include Andreessen Horowitz, Trinity Ventures, Comcast Ventures and Financial Solutions Lab.

Salary Finance is another company operating in the space but doesn’t provide a holistic financial wellness platform, but specifically offers salary-linked loans

Salary Finance

As well as providing a lot of the insights that power the industry, Salary Finance also offers employees salary-linked loans which are cheaper than other sources of credit because they are linked to salary. Employers who partner with Salary Finance typically start by establishing a Financial Fitness Score to understand where their employees need the most help and can then supplement this with financial education tools.

Summary

Beyond the altruistic motivations, the cost to employers of financial wellness is simply too large to ignore. Recouping some of the $500bn per year cost in the US alone seems like low hanging fruit to improve corporate profitability. Fortunately with innovations in fintech, many of the challenges that employees have can be solved through technology and the trusting relationship most employees have with their employers present a unique distribution channel that should be capitalised upon.

Having a financial wellbeing program should not be seen as a cost center but also as a hiring tool to attract talent with this benefit. Financial wellbeing can be turned from a cost center to a profit center.

Appendix — Case Studies

PayPal

Almost a year ago, PayPal created a new Employee Financial Wellness program off the back of a company wide survey that highlighted 65% of employees ran out of money between paydays.

PayPal’s program addressed four main things;

Increased basic wages

Lower the cost of benefits

Allow everyone to be a shareholder

Launch financial planning and education

The results were 4x more engaged employees and 3x less likely to leave. Not only this but there was a decrease in employees who reported running out of money between paychecks, an increase in healthcare enrollment and upgrading of plans as well as a higher rate of 401(k) and employee stock purchase plan enrollment.

The exact financial savings for PayPal will be borne out over the long term and even then might be hard to quantify.

Enrich

Enrich is a workplace financial wellness program provider and it conducted a financial wellness case study which highlighted the below impacts from three companies that used its services.

QLI, a company whose mission is to serve adults that have suffered a catastrophic injury, offered its staff a financial wellness program with the goal of increasing retention. The work QLI does requires dedicated staff and a long-term commitment and employee retention is core to their business model. The program is in its eighth year and the company’s turnover rate of staff is 6%-9%, far lower than the industry average. This low rate keeps costs low and reduces the need for large human resources teams.

Nebraska Furniture Mart also implemented a financial wellness program which has reduced costly 401(k) loans and smooth income for employees working on commission. Its staff turnover reduced to just 20%, a low for the retail industry.

The last example is from Mountain America Credit Union, which provided a wellness program to its employees. The outcomes were increased knowledge about money, an increase of 37% of staff who had an emergency savings account, an increase in savings of $550-$722 and a 79% increase of staff living by a budget.