SotW: Flux - bringing receipts into the digital era

Why do we have to wait for a paper receipt after having used contactless payments?

Startups of the Week ⭐🇺🇸🇬🇧🇪🇺🏆

🚨FATP is now taking submissions for future Startups of the Week here.🚨

If you are a founder working on an interesting fintech, or want to recommend someone, get in touch!

Does it feel strange making a payment via contactless technology, to then subsequently having to wait until a physical, chemically laden paper receipt is printed out? If your answer is yes, keep on reading. If not, keep on reading to have your mind changed.

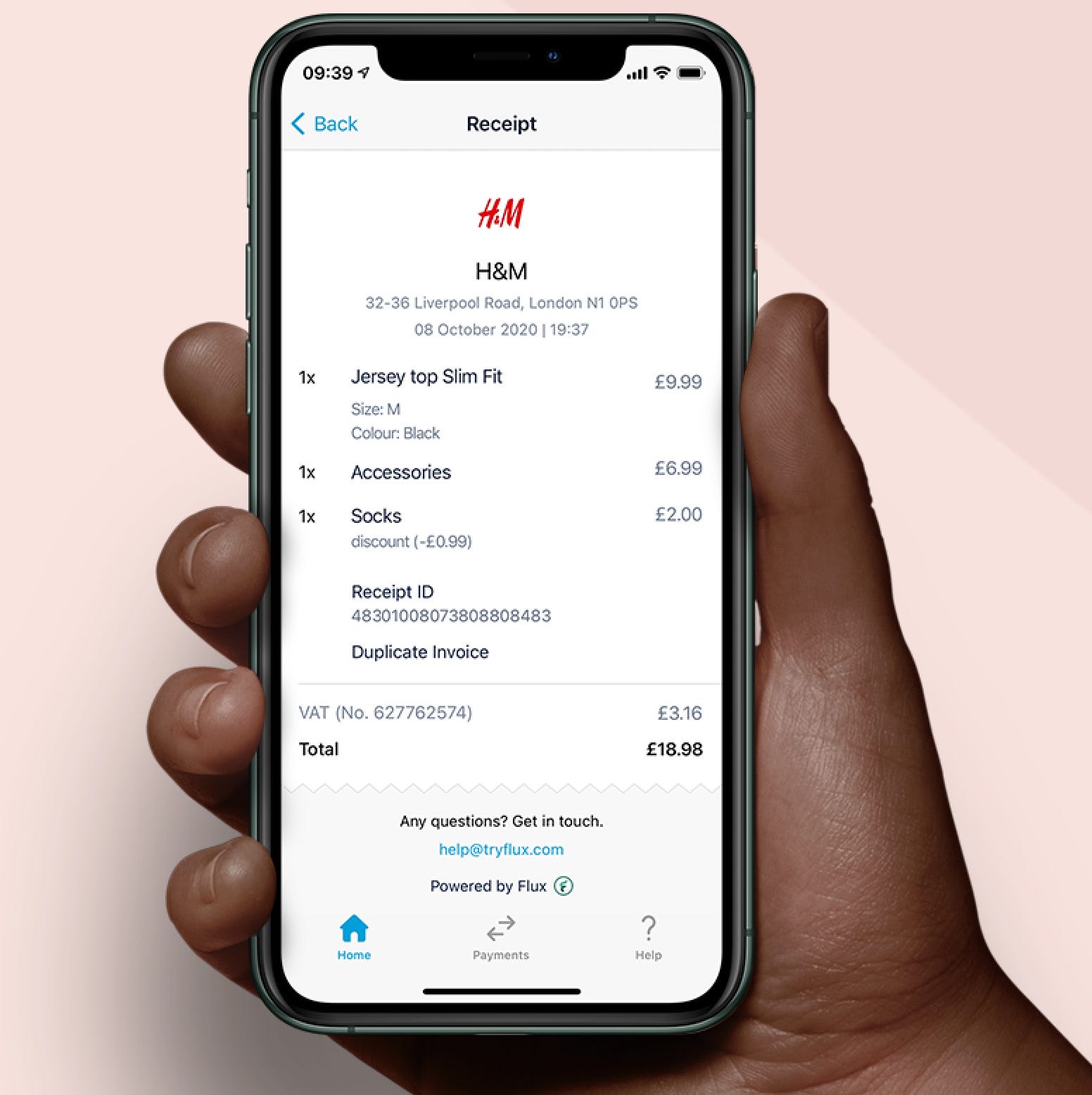

Flux is a digital financial infrastructure company that has developed an API to connect bank payment data with retailers SKU level data in real time. Flux provides consumers with a digital receipt and provides retailers with rewards and customer insights.

Team

The Flux team was founded in 2016 by Revolut alum’s Matty Cusden-Ross, Veronique Barbosa and Thomas Reay. The company went through the Barclays Accelerator program powered by Techstars in 2017.

Product

Flux is a software platform that stitches together two disparate data sources, merchant POS item level data and transaction data from issuer processors, to create a digital receipt. There are three main users of Flux, consumers, retailers and banks.

Consumers

Consumers sign up by linking their bank with Flux to receive digital receipts from participating merchants to the bank’s mobile app. Flux is currently live with three banks, Barclays, Monzo and Starling and merchants include Itsu, H&M, KFC and Pure. In its current form, Flux only works with your bank card and not any credit cards.

The question some consumers may have is why bother?

Firstly, Flux ensures that you always have a receipt when you want to return an item. With statistics showing that 90% of receipts end up in the rubbish, consumers often miss out on refunds, insurance, warranty claims, tax deductions or business expenses due to a lack of proof of purchase. Additionally by linking loyalty points to digital receipts, loyalty points are automatically earned and are not reliant on a consumer having a separate loyalty card.

Retailers

The benefit for retailers include aggregated analytics on consumer spending as well as deeper individual customer insights through merging of online and offline purchasing behaviour. Through linking a bank card, Flux is able to track a customer’s spend at whatever channel it occurs, something that is still important despite the increase in e-commerce volumes. Flux also helps retailers create a single customer view allowing better visibility into key metrics like retention and frequency.

This single customer view can be then leveraged for loyalty and rewards, allowing retailers to personalise offerings and target customers at a very granular level, something that is lacking with social media advertising. Retailers offering digital receipts also appeal more to environmentally conscious consumers and can use this as a key differentiator, a trend that is increasingly becoming important to younger generations.

Banks

The value proposition for banks is a little more nuanced but focuses on having consumers spend more time in the mobile banking app, which increases engagement, with the assumption that a more engaged customer is more loyal and provides additional opportunities for cross-selling. Banks are also able to partner with Flux merchants for rewards and offers, providing the ability to send customers offers from merchants that they actually shop at.

Market

There are over 11bn paper receipts produced each year in the UK, with the number worldwide vastly higher. The Global Thermal Paper market, the key component of paper receipts, is set to be a $5.5bn market by 2025 according to KBV Research, of which POS receipts make up over 75%, and demonstrates its size.

With receipts on average costing between $0.015 to $0.05 each, the direct printing costs alone represent a $165m to $550m opportunity each year in the UK. On top of the direct costs, the environmental costs are also huge. Trees, water, CO2 and the presence of chemical BPA make paper receipts incredibly detrimental to the environment.

Flux’s goal is not only to digitise receipts to lower the cost for merchants, but also to gather SKU level transaction data to power a rewards and loyalty platform. This market is huge, with Fior Markets estimating it reaching $25.26bn by 2027 globally, growing at a CAGR of over 16% from 2020 to 2027.

Consumers are faced with increasing amounts of choice when it comes to making purchase decisions due to the availability of products at our fingertips thanks to mobile and the internet. This means it is harder to create loyalty among consumers, with 70% of consumers stating that it is harder for brands to retain their loyalty than ever before. As social media platforms and internet ads are increasingly becoming more personalised, it opens up the opportunity to provide very personalised reward offers from retailers a consumer actually shops at. Have you ever searched online for a new pair of jeans online, only to then see ads for jeans on Facebook and Google? The monetisation of search data is a large contributing factor to Google’s $1.28trn market cap and $160bn revenues. The monetisation of spending data could be even larger.

However the monetisation of spending data has been more difficult because the spending data purchased and sold by card networks and third parties lacks specificity. Was that £100 Consumer A spent in H&M on new bed sheets, mens jeans or a woman’s skirt? Detail like that matters and without it, it is far harder to fully understand customers. The problem for merchants is the difficulty in gathering the recurring transaction data for their customers individually over time, with all of the different sales channels and payment options. Online, in-store, with different cards, with BNPL providers, checking out online via Google Pay or Apple Pay. The different siloed systems make this a minefield for merchants and so they really lack a holistic picture of consumers and lack the ability to target them, at scale, for specific rewards.

I recently signed up for the new, revamped Google Pay and linked my cards and accounts. With the probable petabytes of data Google has collected on me over the near twenty years of having my email, browser and Android data, it was disappointing to see that the best they could offer me was cashback at Burger King, Gap, Adidas and PetSmart, retailers I haven’t shopped at in years. And I don’t have a pet. If Google is struggling, you can bet all other retailers are too.

Not only is there demand from retailers to better reach their customers, there is also a push from consumers. A survey from Green America found 89% of respondents would like retailers to offer digital receipts. While the survey found an increasing preference for digital receipts among younger generations, the 55+ consumers were evenly split.

Business Model

Flux is aiming to create a huge network by working with issuers processors and merchants to combine their siloed data sets as a neutral third party. The business model is currently B2B, with banks paying to enable digital receipts in their mobile apps to increase engagement with users and to continue to provide the digital experience users demand.

Flux faces a chicken and egg problem as it seeks to onboard both banks and merchants at the same time. Without any merchants onboard, banks will not be interested and vice versa. Since Flux went through the Barclays Accelerator program they found an anchor bank customer in 2017. Flux’s offering fits nicely with the digital offerings of neobanks and they have successfully onboarded Monzo and Starling, two of the largest players in Europe.

Flux has raised $10m+ to date from investors such as Anthemis, PROfounders Capital, e.ventures and the Barclays Accelerator and Techstars programs.

Future

Although currently catering to physical retailers, with online retailers already offering email receipts, there is scope for Flux to be useful to these online retailers. Online has become the playground of fraudsters given the shift to e-commerce in response to the pandemic. With different companies in the payments process between merchants and consumers, transaction data has become opaque and more challenging to recognise transactions on a bank or credit card statement. This causes false positives i.e. when a legitimate transaction is flagged as suspicious. Lloyds found that false positives cost merchants 2.8% of revenue, and Kout, a digital fraud company, estimated this to be $2bn in lost revenue for merchants in the US. Flux can help provide SKU level details to customers which will help mitigate these transactions by providing the consumer the items purchased which are more likely to be familiar to them than an obscure merchant name.

Flux needs to continue onboarding merchants and banks to create the larger network effects needed to provide the most value to each party. The customer experience of discovering Flux and linking your account is currently quite cumbersome and is an area for much improvement. If Flux could leverage the distribution of its partner banks mobile apps and have customers proactively asked to sign up or make Flux easier to discover in-app, that would go a long way to helping onboard more users.

For banks, the promise is to drive engagement with their mobile banking app. The link between engagement and retention or revenues for the bank has yet to be proven. An overloaded and clunky banking app could create a poor user experience but if done correctly, digital receipts have the potential to power a better in-built budgeting or personal financial management tool. Users spending more time on a mobile banking app might also indicate a poor user experience and be due to a more frustrated customer.

Monzo already offers budgeting via categories, the ability to provide more accurate spending analysis would be well received. Spending £100 at a supermarket on food is not the same as spending £100 on alcohol, yet it would both be categorised as “groceries”.

Whilst the promised benefit to the merchant is clear, the proof will be in the pudding. Can Flux provide actionable data to merchants that increases their customer retention and revenues? Time will tell.

Currently the weakest value proposition is to the customer and is really only a nice to have. But, as Flux onboards more merchants its flywheel will kick in and it will provide sufficient data to generate interesting and relevant rewards that a customer will want to engage with.