The $400 unexpected expense myth.

Tweet of the week 🦉

I love this tweet from Brett from Firstround. Knowing the problem by going deep is a guaranteed way to succeed. When I think of the different challenger banks out there, how well do they truely understand the customer problem? How much real customer research have they done?

If you enjoy reading this, please subscribe and share with your family, friends and other fintech enthusiasts!

Recent News 📰

🇺🇸 There is an often quoted statistic in financial services that a large share of Americans can’t cover a $400 expense. This however is a misinterpretation of the survey. The report found 61% would cover a $400 unexpected expense with cash so the incorrect conclusion drawn was that the other 39% could’t come up with the money. This is despite the fact that evidence shows “76% of households had $400 in liquid assets after monthly expenses”. Link.

🇬🇧 Tech Nation has announced the 31 fintechs it has selected for its Fintech 3.0 growth program. The list highlights the top fintechs in the UK. 60% are based outside of London, 29% have a female founder, 20% are in the insurance space and 17% in lending.

Funding 💵

🇪🇺 Exabel, a startup providing data analytics for risk management teams in the asset management industry has raised $3.6m.

🇪🇺 Russian technology firm Yandex is acquiring Russia’s digital-only bank Tinkoff for $5.5bn.

🇬🇧 UK based TrueLayer has raised fresh funds in a Series C led by its existing investors Anthemis, Connect Ventures, Northzone and Temasek. Reports about the amount vary, with some sources quoting $25m but PitchBook has reported the round as $60m. Mouro Capital, the renamed and relaunched VC previously known as Santander Innoventures, joined as a new investor.

🇬🇧 Mouro Capital has also invested in Uncapped’s $26m round alongside Seedcamp, Taavet Hinrikus and White Star Capital. Uncapped provides revenue based financing for companies looking to grow. They provide £10k-£2m in funds.

🇬🇧 London based CloudMargin has raised a $15m series B from new institutional investors Citigroup, Deutsche Bank and exchange Deutsche Borse Group.

🇺🇸 Petal, the credit card disruptor, has raised a $55m Series C led by existing investor Valar Ventures.

🇺🇸Robinhood extended its Series G from $200m to $460m at an $11.7bn valuation.

🇺🇸In a further demonstration of the increasing verticalisation of the challenger bank space, Greenlight Financial Technology which provides an app and debit card for kids has closed a $215m Series C at a $1.2bn valuation. The round was led by Canapi Ventures and also included DST Global, Goodwater Capital and Bond Capital.

Challenger Banking 🚀

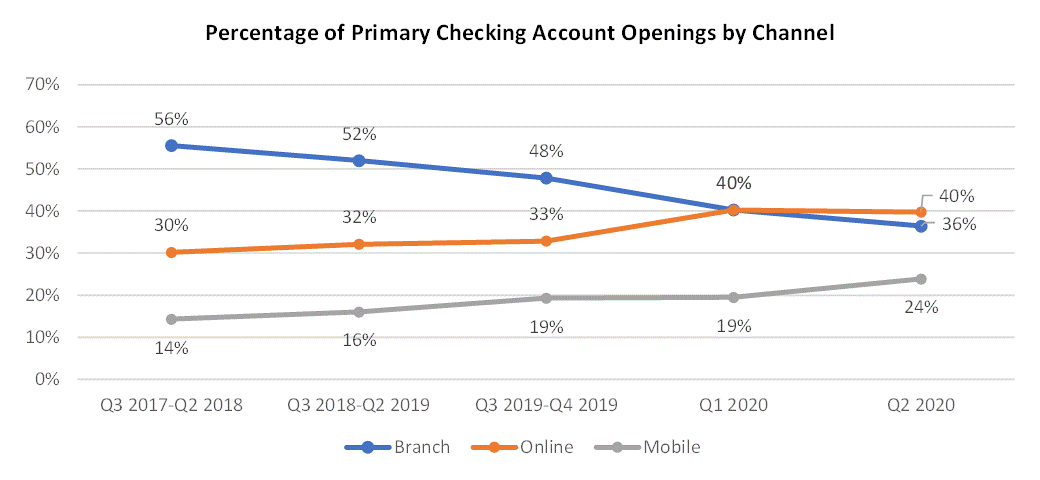

🇺🇸 Cornerstone Advisors has found that digital account openings of primary bank accounts surged before the Covid crisis, in the second half of 2019 and has continued.

🇺🇸 Exiting news from Privacy which has teamed up with 1Password to let you create virtual cards in your browser for when you are shopping online. Virtual cards allow for increased privacy by creating a virtual credit card whose details you use when paying instead of your actual card information. Merchants never have access to your real card details. The partnership with 1Password allows users to easily do this from a browser extension very quickly at checkout. Link.

🇺🇸 Cross River Bank raised $250m in consumer deposits in 15 days after partnering with Mantl, an fintech with digital account opening software. The deposits enabled Cross River Bank to become a PPP lender. Link.

🇺🇸 MoneyLion is switching from a bundled subscription pricing structure to segmented pricing structure to entice more customer. Link.

🇺🇸 Walmart is partnering with Goldman Sachs to offer its marketplace sellers credit. The lending will come from Goldman’s Marcus brand and be for $10,000 to $75,000 with increases to come in the future. Both Amazon, Square and Shopify already provide similar credit lines to merchants on their platforms. Interestingly Amazon’s offering is powered by Goldman and it seems they are reusing the technology with a competitor.

🇺🇸A digital banking startup focused on middle class Americans has launched. One, founded by former PayPal and Capital One executives aims to fill a gap in a bespoke product for them with saving, spending, sharing and borowing in one account with one card.

Traditional Banking 🏦

🇺🇸 The misery at Wells Fargo never seems to stop as CEO Charlie Scharf apologised for his June comments in which he blamed the lack of diversity in the industrry on a “very limited” talent pool. Such nonsense and I for one will be looking for an alternative checking account provider. Please don’t judge that I am still with WF.

🇺🇸 On the opposite end of the spectrum is Citi has pledged $1bn in incentives to help close the racial wealth gap and provide economic resources for people of colour.

Fintech Infrastructure 🚧

🇪🇺 Tink, the Swedish open banking platform has acquired UK based OpenWrks.

🇬🇧 Cloud core banking provider Thought Machine has named former HSBC operating officer Andy Maguire as its chair. This brings a great degree of experience to the fintech.

Payments 💰

🇪🇺 The EU is debating forcing Apple to open up the NFC functionality to allow rival payment providers, as reported by Bloomberg.

🇺🇸 Mastercard has expanded its digital card program with PTS, Fiserv, CoreCard, FIS, i2C, Galileo, Marqeta and TSYS. The expansion means their customers will get almost instant access to card information, giving them peace of mind to make secure transactions. Link.

🇺🇸 Stripe has partnered with Salesforce to power their cloud-payment system. Salesforce customers can set up payment platforms with Stripe’s technology.

Regulatory Corner 🔬

A great post from Simon Taylor of 11:FS on the FinCEN files - “What the FinCEN files leak means for banks”.

Longer reads 📜

“Why Self-driving money is so hard” - Alex Johnson

🙌🏻 This piece by Alex is an excellent summary of the struggles with automated personal financial management and self-driving money which has been spoken about by Wealthfront and Credit Karma. Look out for my post on this which is coming soon and builds upon the ideas Alex wrote about and that I share.

“The AWS of Finance” - Marc Rubenstein

“Even when they lost their jobs, immigrants sent money home” - NYT

“FinTech: The 2020s” - John Street Capital

“What will drive capital markets firms to migrate to cloud in 2020 and beyond?” - Finextra

“Bailout Tracker” - ProRepublica

🙌🏻 This bailout tracker tool follows where the taxpayer money has gone from the bailout of the financial system. The data shows the government has realised a $110bn profit as of August 2020. The image of financial services took a dramatic hit during the great financial crisis and has never really recovered. Fintech experienced a massive growth spurt in the aftermath but I thought it was important to note that the US taxpayer has profited from the bailout. Two of the largest losses were from General Motors and Chrysler according to the data.

Startups of the Week ⭐🇺🇸🇬🇧🇪🇺

All star US cast of startups this week!

🇺🇸 EquityBee is a platform for early employees of startups to get the capital they need to exercise their stock options. The company allows EquityBee investors to share in the upside of these stock options alongside the startup empoyee. This is a big problem for early stage employees whose wealth is on paper and they often lack the capital needed to exercise their valuable options. EquityBee has raised $8.3m to date, with a timely $6.6m Series A in February from investors including Battery Ventures, LocalGlobe and WeWork founder Adam Neumann.

🇺🇸 The Zebra is a comparison engine for car insurance and connects to 200 trusted insurance companies. Price comparison websites are very popular in the UK for financial products but given the fragmentation of the US market with its state and federal regulation, they have had a harder time coming to market. The Zebra boasts Accel, Mark Cuban and MoneySupermarket (a UK price comparison website) amongst its investors.

🇺🇸 Esusu is helping low-to-middle income customers report rental payments to credit bureaus to boost their credit scores. Low or no credit scores are a source of much financial distress for the low-to-middle income segment who often find themselves excluded from traditional sources of capital and forced to take credit with high interest rates or face numerous overdraft fees. Esusu has Kleiner Perkins and Plug and Play as investors

Please get in touch to share your thoughts and comments!

Follow me on LinkedIn and Twitter.

Michael