UK 169 vs 107 San Francisco

Fintech score 2020 YTD

Tweet of the week 🦉

Another fintech twitter thread masterclass from QED’s Frank Rotman. There is room for digital banks but they must focus on solving customer problems and adding value.

This week has seen a bunch of rounds raised from US fintechs as well as UK news from challenger banks. Enjoy!

If you enjoy reading this, please subscribe and share with your family, friends and other fintech enthusiasts!

Recent News 📰

🇬🇧 Innovation agency Nesta named Mojo Mortgages, Moneybox, Plum and Wagestream as winners of its £1.5m open banking competition. Link.

Funding 💸

🇬🇧 UK fintechs take the top spot in terms of deal count with 169 in 2020, although the total investment of $3.6bn was behind the $5.1bn that San Francisco’s 107 deals attracted.

🇺🇸 Clair has raised $4.5m to help facilitate instant payment for gig workers. Among the investors were Upfront Ventures, Walkabout Ventures, Founders Collective and a cast of angels.

🇺🇸 M1 Finance has raised a $45m Series C from Clocktower, Jump Capital and Left Lane. M1 Finance is building out a super app to automate personal financial management.

🇺🇸 Extend, an extended warranty startup, has raised $40m in Series B led by Meritech Capital which also included PayPal Ventures.

🇺🇸 Argyle, the Plaid of employment records, raised $20m Series A led by Bain Capital Ventures and also Ian Kar and Nik Milanovic’s syndicate.

🇺🇸 Alpaca has raised a $10m Series A for its commission-free trading white label solution. The round was led by Portag3 and included existing investors Spark Capital and Abstract Ventures.

Challenger Banking 🚀

🇪🇺 N26 is exploring additional capital raises in 2021 despite a recent round which valued the company at $3.5bn. There seems to be a rush to raise capital for challenger banks as they look to continue their expansion and find their way to profitability.

🇪🇺 Russian digital bank Tinkoff and Yandex have abandoned their $5.5bn deal after they couldn’t agree to terms.

🇬🇧 A busy week for Revolut in which it launched its offering of a 5% interest rate for US savers (link) and is pursuing regulatory license in both the UK and the US.

🙌🏻 Check out this fantastic twitter thread by US bank regulation expert Matt aka @regulatorynerd.

🇬🇧 UK fintechs ThoughtMachine and Curve are partnering. ThoughtMachine’s Vault will power Curve’s new credit and loan solution. Curve Credit will allow users to pay for purchases in instalments, joining the BNPL craze. Don’t you just love a fintech-fintech partnership! Link.

🇬🇧 Two former Barclays exec’s are launching Pennyworth, a digital bank focused on young professionals and middle managers. Pennyworth will provide financial planning, savings, loans and overdrafts.

🙌🏻 This trend of vertically focused digital banks is increasing but being able to add value to the segment that is being targeted is still difficult as these services are available through traditional banks already.

🇬🇧 Starling Bank is looking to build on it’s lending program from last year in which it lent its deposit base through Zopa and Funding Circle. It is rumoured to be looking at acquiring loan originators.

🇬🇧 Plaid and PensionBee are teaming up to push for open standards within the pension industry to improve financial decisions.

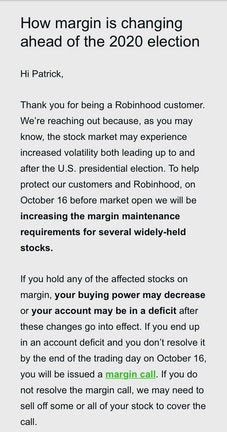

🇺🇸 A bad week for Robinhood as an internal probe found that hackers had hit 2,000 accounts and siphoned customers balances. In a separate issue, it email customers and gave them less than 24hours to increase cash in their account for increased margin calls due to expected volatility in the run up to the election. Link. h/t Patrick McCormick

Traditional Banking 🏦

🇺🇸 Both JP Morgan and BlackRock chiefs have expressed interest in deals in the wealth and asset management spaces. Link.

🙌🏻 The wealth/asset management space has become increasingly appealing to banks due to the lack of capital required to operate such a business. Banks also benefit from scale, just look at BlackRock, although increased competition is putting pressure on fees. I wonder if some fintechs are in play or they will look to larger more established targets.

🇺🇸 US bank results are in. Check out this great summary from Adam Davis.

🙌🏻 TL;DR banks beat low expectations, consumer banking hit but IB and wealth management businesses performed well

🇺🇸 Chase is introducing a new account for parents and children in collaboration with Greenlight.

🇺🇸 BofA has introduced Balance Assist, a new way for customers to manage short term borrowings. They can borrow up to $500 for a flat $5 with repayments made in three equal installments over 90 days. This is on top of “SafeBalance Banking” which only allows customers so spend the money they have and its “Keep the Change” roundup program.

Fintech Infrastructure 🚧

🇬🇧 PayPal is launching a BNPL service in the UK, taking on Klarna and AfterPay. It could leverage its superior brand recognition amongst consumers and make quick headway to attracting customers.

🇺🇸 Fed is making progress with its FedNow instant payment program and is looking for pilot participants this past week.

Payments 💰

🇺🇸 Stripe has acquired Lagos based Paystack in a deal worth more than $200m. Stripe led the $8m Series A of Paystack back in 2018.

Longer reads 📜

5 Bank and fintech partnership ideas to generate revenue - Ron Shevlin, Forbes

Banking as a Service: the future of financial services - Simon Taylor, 11:FS

Can banks catch up on infra? - Cokie Hasiotis

🙌🏻 I agree with Cokie that fintech infrastructure players will need to change to compete with banks. Partnering with each other to bring end to end solutions to other fintechs and banks would seem logical. Think of it like banking-in-a-box if you had leading digital account opening software + leading cloud core provider + leading digital identity and KYC software + leading card issuance provider + leading AML software. Like BaaS but with each company being a specialist and expert in one area.

Buy Now Pay Later - Marc Rubinstein, Net Interest

To lend or not to led - Yusuf Ozdalga, QED

Startups of the Week ⭐🇺🇸🇬🇧🇪🇺

UK based Zilch has joined the BNPL craze with its virtual card which allows you to split any purchase into four easy payments over six weeks. They have over 5,000 signed up for the wait list as well as a 4.7/5 TrustPilot rating. Zilch has raised $10m to date and was started by serial founder Phillip Belamant. The approach taken by Zilch allows any payments to be split compared to the larger players in the space which are integrated in the checkout process of merchants so takes longer to scale. Visa and Masercard both offer installment solutions but have yet to gain much traction but expect this to change as the sector is 🔥 right now.

The BNPL is set to grow 9% in 2020-2021 to a $750m market size according to IBISWorld and is benefitting from the huge growth in ecommerce post-covid which looks set to continue. The industry is dominated by platforms Afterpay ($19bn market cap), Klarna ($10.65bn) and Affirm ($10bn rumoured IPO valuation).

US based Lendtable is helping customers take advantage of their employers 401(k) matching policies by giving them a cash advance to put into their 401(k). This is then matched by the employee and Lendtable takes a small service fee. For an individual with a $50k salary and an employer match of $1 for $1 on 5% of salary, Lendtable could earn them $2,375 they would otherwise have missed out on.

The market for Lendtable is huge, as Financial Engines found 1 in 4 employees aren’t saving enough to receive their full match from employers and amounts to $24bn annually!

It was founded by serial entrepreneur Sheridan Clayborne and Mitchell Jones whose previous employers include Dropbox, Facebook, JP Morgan and Goldman Sachs. Lendtable is in the S20 YC batch and has raised $8.5m to date from investors such as Partech, Socii Capital, Softbank as well as YC and angel investors.

Find out more on employer matching here.

Please get in touch to share your thoughts and comments!

Follow me on LinkedIn and Twitter.

Michael