Banking needs to come out of the shadows

Tweet of the week 🦉🏆

Jason does an excellent job breaking down the “shadow” financial live that takes place outside the walls of traditional financial institutions from the FICO report. My main takeaway was how complicated people’s financial lives have become. For some time consumers have moved away from having one bank for all their financial needs but this has really accelerated in the last ten years with the unbundling of financial services and the creation of new financial products with millennials are at the forefront of this.

It is no wonder that consumers are not engaged with their financial lives and don’t always make the best financial decisions. It is just so complicated, time consuming and stressful to manage as many as 9 financial products with different features and functionality on different mobile, web and in branch. It was difficult even before the added effects of Covid.

I firmly believe that all of these accounts need to be connected to a central hub that can help reduce the stress of management and give the consumer a holistic picture of their current financial situation at a minimum, something I have previously written about. This would bring banking out of the shadows and increase transparency and access to information. In the best case, it would provide automated and actionable insights on how they can make better financial decisions so they can achieve their individual level goals. This automation of banking or self-driving money must exist in an open ecosystem so consumers can connect any accounts they want, and not just limited to accounts at one institution.

For this to happen, infrastructure needs to be built to easily move money. Astra is working on this and recently officially launched its platform. But more importantly it involves a consumer first mindset at financial institutions that I don’t see existing currently. Banks still don’t want you to venture outside of their ecosystem (we need more Google and less Apple thinking) and would prefer to funnel you into ill-fitting products they can generate revenue from. If/how/when this changes is anyone’s guess but technology isn’t what is holding it back.

If you are overwhelmed by content to read online, you should check out Joggo, a content curation platform to both organise and discover new content.

You can save articles, newsletters, tweets into Playlists to share as well as discover new content through following Playlists from the greatest minds on earth.

Jogs are quick summaries of content to act like a preview or trailer to help you know what to spend your time reading as well as recall information.

Check it out and sign up to the waitlist here!

If you enjoy reading this, please subscribe and share! 🙏

Funding 💸

There were 50 deals in the fintech space across the US and Europe with total investment of ~$700m. Some highlights are below.

🇪🇺 The latest Klarna rumour is a raise of $1bn at a $31bn valuation.

🇪🇺 Penta has raised an additional €7.5m, topping up its Series B from finleap and AMB Amro Ventures.

🇪🇺 Scandinavian subscription terminator Subaio ha raised €4m from former Mastercard executive Javier Perez.

🇪🇺 Zelf has raised a $2m pre-seed round led by 3VC and included Chris Adelsbach and Hard Yaka.

🇬🇧 Atom is raising £40m from its existing investors ahead of its 2022 IPO.

🇬🇧 Sokin, a global payment solution for consumers and businesses has raised money from former footballer Rio Ferdinand.

🇬🇧 Middleclass challenger bank Monument has raised £28m from angel investors.

🇬🇧 Payaca is raising £1m for its solution to help tradespeople manage payments and workflow.

🇬🇧 Orka has raised £29m in debt and equity from Sonovate, British Business Bank and Peter Searle as it looks to fuel its growth

🇬🇧 TreeCard has raised $5.1m in a round led by EQT Ventures for its reforestation debit card.

🇺🇸 EarnUp raised $25m in a Series B led by Bain Capital Ventures and also included Blumberg Capital, Flourish Ventures and SignalFire

🇺🇸 Finix raised a $3m round via an SPV for 80 underrepresented investors, putting words into action to include the diversity of their investor base.

🇺🇸 Toast is considering an IPO which could value it at $20bn according to the WSJ and have hired Goldman Sachs and JP Morgan.

🇺🇸 FundGuard has raised a $12m Series A led by Blumberg Capital and LionBird.

🇺🇸 Alkami is readying for a $3bn IPO according to Reuters.

🇺🇸 Episode Six has raised $30m in capital for its payments API from existing investors Anthos Capital, HSBC, Mastercard and SBI Investment.

🇺🇸 Petal has closed a $127m debt round from Silicon Valley Bank and Trinity Capital.

🇺🇸 EquityBee has raised $20m in a Series A led by Group 11 and included Battery Ventures, Oren Zeev Ventures and ICON Continuity Fund.

Challenger Banking 🚀

🇬🇧 The first Black British challenger bank Atmen is launching imminently with a remittance service and prepaid debit card.

🇺🇸 Varo Bank is introducing Varo Believe, a credit building card that reserves money spent from a linked Varo bank account to a secure Vault Account to pay credit card balance on time with no upfront deposit or fees and payments are reported to the credit bureaus to improve credit scores.

🇺🇸 In just four months Step has hit 1 million users, demonstrating the power of social media influencers.

Traditional Banking 🏦

🇪🇺 BBVA will use Google Cloud’s security platform Chronicle to protect it from cyberattacks.

🇬🇧 Lloyds will integrate Mastercard’s Open banking software to allow customers to pay their credit cards with PISP payment.

🇬🇧 More open banking news as NatWest is using the technology to power Payit, allowing businesses to send payments to consumers directly for refunds, compensation and emergency cash payments instead of cheques and bank transfers.

🇺🇸 Wells Fargo is selling its asset management arm to private equity firms in a bid to cut costs and streamline around its core retail business.

🙌🏻 FATP Take - This is in contrast to other firms which are investing into asset management such as Goldman Sachs (Marcus Invest) and Morgan Stanley (acquiring Eaton Vance) as the industry consolidates to gain economies of scale.

Fintech Infrastructure 🚧

🇺🇸 Treasury Prime is partnering with Marqeta to add modern card issuing to its BaaS API, allowing companies to embed banking services and card issuing in one API.

Payments 💰

🇪🇺 The European Payments Initiative is seeking infrastructure partners to help build its rival to Visa and Mastercard.

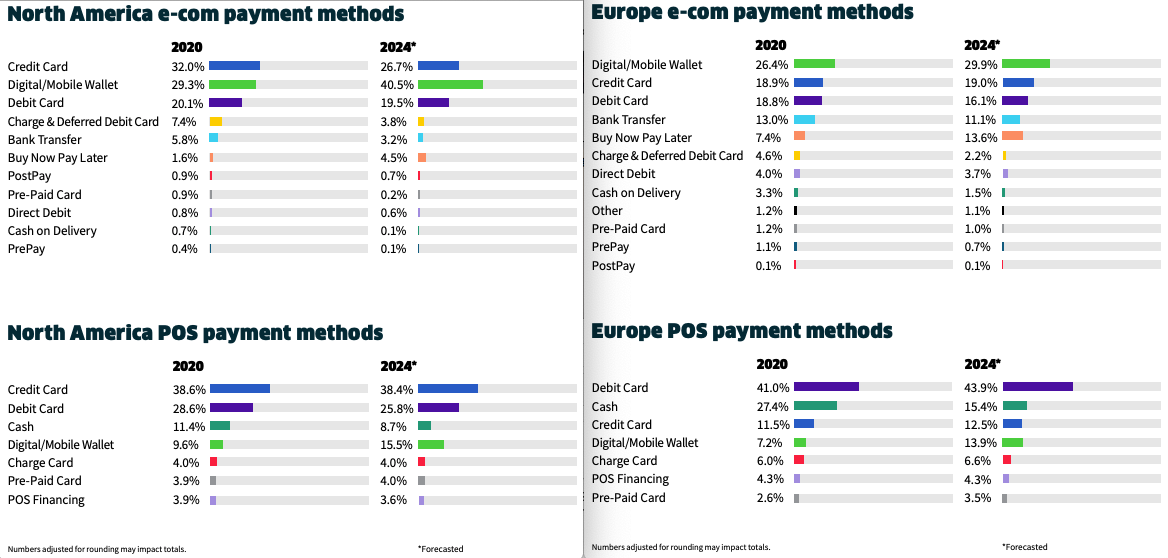

🇬🇧 Worldpay’s 2021 Global Payment Report indicates BNPL will account for 10% of UK e-commerce sales by 2024 and globally, mobile wallet use exceeded cash for in-store payments which is hardly surprising given the pandemic. It will be interesting to track what happens when things get back to a new “normal”.

🙌🏻 FATP Take - Other notable highlights include the increasing penetration of digital wallets (44.5% of all e-commerce transactions by volume) and their rapid adoption in the US (nearly 30%, up from 24% in 2019). BNPL is expected to double to 4.2% of all transactions by 2024.

🇺🇸 AfterPay has secured a huge partnership with Stripe, giving them a distribution platform via merchants using Stripe to offer customers the option of paying later. They are also integrating with Squarespace to offer integration to e-commerce customers in Australia, New Zealand and the US.

🇺🇸 Visa and Mastercard are looking to raise swipe fees for credit-card purchases in April, including for online purchases where the risk of fraud is higher, according to WSJ.

🇺🇸 Affirm is partnering with holiday rental platform Vacasa to bring BNPL payments to travel in what seems like a good fit. Watch out for Airbnb following suit. Affirm is also launching a debit card with BNPL functionality as it pushes beyond its checkout button offering towards a fully fledged banking experience.

🙌🏻 FATP Take - Affirm seems to be increasingly targeting larger purchases rather than smaller impulse purchases which is likely to have higher loyalty, building up partnership like with Peloton. Zilch is taking a similar approach and you can read more about them here.

🇺🇸 Intuit has sued Visa and Mastercard over price fixing on interchange and card scheme fees.

🇺🇸 Klarna and Square both released earnings this week for 2020. Klarna reported FY 2020 of GMV $53bn (+46%), revenue $1.1bn (+40%), loans $4.5bn (+45%), write offs 6.1% (down from 6.3%), 86m active consumers and 250k retailers. Square Q4 2020 saw profit +52% yoy to $804m, Cash App profit to $377m (+162% yoy) and Seller Ecosystem $427m (+13% yoy). Cash App had 36m MAUs (+50% yoy) with $5 CAC and $41 gross profit per month per active customer.

🇺🇸 Earlier this week the US Federal Reserve system used to execute payments went down for several hours causing a backlog with ACH and Fedwire.

Longer reads 📜

Meme stocks and FOMO are attracting millions of newbie traders - Business Insider

Underbankers - Alex Johnson

Talking Seed with Sequoia - Sequoia

Are sports cards the future of retail investing - Justine and Olivia Moore

The big fight: banking vs tech companies - Dharmesh Mistry, Fintech Futures

One year into the pandemic, millions of Americans still struggling - Financial Health Network

Are fintechs really here to fix users’ finances? - Jason Mikula

Kabbage Co-Founder Muses On Alt Lending, Fintech Trends, And More - Cheryl Munk, Forbes

Your feedback is a 🎁, please give below 🙏

Good || Bad || Needs Improving

Follow me on LinkedIn and Twitter.

Michael