Fintechs benefit from playing in a sandbox

Tweet of the week 🦉

The above tweet from Will Quist sparked a lot of debate on twitter, with experts coming down on both sides of the arguement.

A BIS report looking into the effect of regulatory sandboxes found that firms entering the FCA sandbox have a higher probability of raising funding and increased the average amount of funding 15% related to startups that didn’t join.

Quick quiz - What country has cash transactions making up 4% of total? No cheating. Leave a comment with your answer.

If you enjoy reading this, please subscribe and share! 🙏

Recent News 📰

🇪🇺 A fantastic map of the Swiss fintech ecosystem by Swisscom.

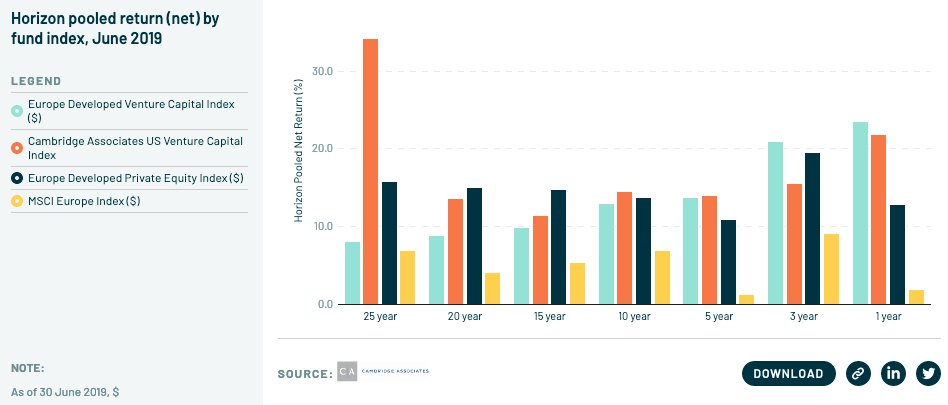

🇪🇺 Over 1,3 and 5 years, European VC has matched or outperformed US VCs according to Cambridge Associates, with data to June 2019.

🇺🇸 Data from the Financial Health Network 2020 report shows some positive signs of improved financial health but a large racial disparity remains.

Funding 💸

🇪🇺 Aidexa, an Italian challenger bank, raised a €45m seed from Generali Group, Banca Sella and 360 Capital Partners.

🇬🇧 Seedcamp, the UK based European accelerator program, raised a £78m Fund V.

🇬🇧 Origin Markets, the end-to-end digital debt issuance platform, raises a $7m Series A from Deutsche Borse and Luxembourg Stock Exchange.

🙌🏻 FATP Take - I had the pleasure of interning with the rockstar team at Origin in 2019 and it was an incredible experience. There is a lot of exciting talk in the fintech space about owning the system of record or truth file, as Frank Rotman says. Origin is doing just that for the $130trn global bond market and if they own the issuance data, many services can be built on top. Congrats to Raja, Rob and the team! Check out this interview with CEO Raja.

🇬🇧 Three UK fintechs are looking to raise. Starling Bank (£200m), Curve (£76m from existing investor IDC Ventures) and GoCardless (£100m with Bain Capital Ventures leading) are all simultaneously trying to raise.

🇬🇧 Railsbank, the Banking-as-a-service platform, raised $37m from MiddleGame Ventures, Ventura Capital and Clocktower.

🇬🇧 PFM app Snoop has crowdfunded £10m from 1,700 investors on Seedrs.

🇬🇧 United Fintech, a firm looking to buy capital market fintechs to re-sell to financial institutions made its first acquisition, NetDania.

🇬🇧 Glint Pay, a fintech enables consumers to store, spend and save their wealth in gold raised £2.5m

🇺🇸 Arcus, the fintech-as-a-service company, raised a round of an undisclosed amount from Citi Ventures.

🇺🇸 Sheel Mohnot and Jake Gibson, of 500 Startups and NerdWallet respectively, have raised a $75m debut fintech fund. Better Tomorrow Ventures will definitely be one to watch as these two are among the most respected fintech investors in all of fintech Twitterverse and beyond. Check out their Techcrunch interview.

🇺🇸 Lightico, a digital customer interaction platform, raised $12.6m from Oxx, Mangrove Capital Partners and Capital One Ventures.

🇺🇸 AppBrilliance, the open payment technology, raised a $3m seed from Studio VC.

🙌🏻 FATP Take - The company offers a product which is similar to account-to-account payments in the UK which is a hot space right now. Merchants get their funds immediately without the need for going through card networks. A space to watch IMO.

🇺🇸 Truebill raised $17m in Series C funding which included new investor Bessemer Ventures.

Challenger Banking 🚀

🇬🇧 UK credit scores are being boosted with payments for council tax, Netflix and Spotify being incorprorated by Experian through Open Banking.

🙌🏻 FATP Take - This will improve the score for over half of people using it, with 1 in 10 moving up an entire score band. Alternative data could make a meaningful difference to credit scores with new behaviours being linked with higher creditworthiness and could result in lower cost of borrowing for consumers.

🇺🇸 Robinhood was slapped with a class-action lawsuit for failing to inform investors about a stock being halted.

Traditional Banking 🏦

🇬🇧 HSBC is working with Young Money, a financial education charity, on a platform to improve financial literacy during the UK’s second national lockdown.

🇺🇸 Unsurprisingly, a survey by the Federal Reserve found banks are tightening underwriting standards for consumer and commercial loans.

Fintech Infrastructure 🚧

🇬🇧 Standard Chartered Bank is moving its systems and customer applications to the cloud courtesy of Amazon Web Services. Another fintech win for AWS.

🇬🇧 Open banking connectivity firm Yapily is expanding into Germany.

🇺🇸 Dave, a mobile banking app, moved from BaaS provider Synapse to Galileo in a sign of further trouble for the a16z backed Synapse.

🇺🇸 Piermont Bank and Treasury Prime are entering into a strategic partnership to enable fintechs to embed Piermont’s payment and banking solutions using Treasury Prime’s APIs. An interesting tweet thread by Alex Johnson pondering if one of these partner banks will buy a banking-as-a-service startup.

Payments 💰

🇬🇧 The OBIE, Open Banking Implementation entity, has launched a consultation about Variable Recurring Payments (VRP) and Sweeping. Reader beware, you may find those links dull so feel free to skip and get the summary below. This could be a real innovation accelerant for payment fintechs in the UK.

🙌🏻 FATP Take - Currently for payments in the UK, consumers can move money almost instantly and for no cost. But for the underlying entity, this movement of money is not cheap. Whether it’s direct debit, credit cards or the newer Payment Initiation Service, all have their downsides including a lack of control, user friction and high cost. VRP could solve these challenges by allowing variable amounts to be taken on irregular intervals with higher security and control for the user. VRP and Sweeping, the process of automatically moving funds between two accounts, will dramatically lower the cost of processing payments and could see more automated moving of money and better payment experiences for users.

🇬🇧 The above chart from Accenture has been doing the rounds and shows the disruption to payments revenue of banks since 2015 with regulation changes.

🇬🇧 Judopay has signed a big new customer, the UK government. Seeking to adopt digital payments in the public sector, Judopay will lead this effort.

🇺🇸 Zelle reported it passed the one billion transaction mark in the year ending September with huge growth due to covid.

🇺🇸 Google has released an app that will allow lenders to remotely lock a mobile phone if loan payments are not made. It was developed to help Safaricom in Kenya but could have wider implications. Would you take a lower interest rate if this feature was enabled?

🇺🇸 Visa is rolling out its Fintech Partner Connect program in Europe, giving financial institutions and merchants access to its fintech partners.

Regulatory Corner 🔎

🇪🇺 The Financial Stability Board, the international body monitoring the global financial system is looking to develop a coordinated approach arising from the increasing outsourcing and third party relationships that are more prevalent recently.

🇺🇸 Congress issued a letter to the OCC urging it against “unilateral rulemaking” which has been fintech friendly. 👎

Longer reads 📜

Financing the American Home - Marc Rubinstein

Finding startup ideas and building in heavily regulated spaces - First Round interviews Ayo Amojola

The impending credit card boom - Ron Shevlin

🙌🏻 FATP Take - Whilst the popular narrative is Gen Z prefer’s debit, Ron lays out data and arguments for the opposite. Credit building fintechs will help the growth of credit cards and its a profitable business for banks.

Neobanks may have lost their shine, but the fintech revolution is far from over - Rory Stirling

🙌🏻 FATP Take - I completely agree with Rory here and I see self-driving money as that software layer that sits in between users and back end financial services and takes away the headache of personal finances. More on my thoughts here

Is fintech Series A market hot or overhyped? - TechCrunch

Why the Bank of England should give everyone a free account - Yanis Varoufakis

What the Goldman BaaS Stories Missed - Jason Mikula

Startups of the Week ⭐🇺🇸🇬🇧🇪🇺

You can check out last month’s featured startups here.

🙋If you are working on any exciting fintech startups, I would love to connect with you so drop me a message.

🇪🇺 Gemms is a financial operating system for SMBs. It leverages open banking and AI and bundles banking, expenses, invoicing, accounting and taxes into one tool. It works with SMBs existing services but provides a one-stop-shop to manage existing processes.

Gemms was founded by Ivan Maryasin and Andrey Korchak. Ivan has a deep background in the SME space from his time at Penta and Andrey built backend infrastructure for a SME neobank Tochka.

🇺🇸 SeaBass is a no code challenger banking platform. Combining the two powerful movements of no-code and banking-as-a-service, Doug Bobenhouse is taking an approach that he dubs “Shopify for banking”. SeaBass allows the creation of white-label fintech apps with modern, digital, best in class vendors. This will further democratise the ability to create and embed financial services by removing the need to have a developer and use vendors that are digital first.

Doug started his fintech career back in 2000 at a prepaid card company where he got insights into the different use cases for prepaid cards as well as the value of understanding spending data and its scalability. He started Synchology in 2009 to offer a platform for non-financial brands to offer debit and savings accounts but the offering was too early. Doug bringing a depth of experience to SeaBass and is hitting the market at the right time.

Your feedback is a 🎁, please give below 🙏

Follow me on LinkedIn and Twitter.

Michael